Moving to America can be an exciting but also stressful time. There are a lot of things you need to take into account and prepare for such as finding a place to live, getting a job, and dealing with culture shock. One of the most important things you need to do is to make sure you are financially prepared for your move. Here are 10 tips on how you can do just that.

1. Have at least 3-6 months of living expenses saved up before you make the move. This will help you cover the costs of rent, food, utilities, transportation, and other necessary expenses while you are looking for a job.

2. Get your finances in order before you leave. Make sure you have paid off any debts and have enough money saved up to cover your relocation costs.

3. Research the cost of living in your destination city. Different cities in America have different cost of living expenses. For example, New York City is known for being one of the most expensive places to live in the US while smaller cities like Wichita, Kansas have a much lower cost of living.

4. Find out if your current health insurance will cover you in America. If it doesn’t, look into getting health insurance through your job or purchasing a private plan.

5. Once you have arrived in America, open up a savings account and start setting aside money each month so that you have an emergency fund to fall back on if needed.

6. Start building up your credit score by getting a credit card and using it responsibly or taking out a small loan and making your payments on time each month.

7. Know your rights as an immigrant. Familiarize yourself with organizations that can help you with legal assistance or any other needs you might have.

8. Educate yourself about America’s taxes system and make sure you are paying your taxes correctly so that you don’t get into trouble down the road.

9. Learn about American banking and investing so that you can make the most of your money once you arrive in the US .

10. And finally, don’t forget to pack some cash! Although most transactions in America are done electronically these days, there are still some situations where cash is king (think tipping cab drivers or buying snacks from street vendors).

Making the decision to move to America can be both exhilarating and daunting but with proper preparation, it doesn’t have to be overwhelming.. Finances are one area that needs careful consideration before taking the plunge but following these 10 simple tips will help ensure that you are financially prepared for whatever comes your way during your transition into life in the United States.

Applying for a visa to the United States can be a daunting task. There are many different types of visas, and the application process differs depending on the type of visa you are applying for. In this blog post, we will provide a checklist of required documents for the most common type of US visa: the nonimmigrant visa.

The following is a list of required documents for the nonimmigrant visa application:

1. Passport

Your passport must be valid for at least six months beyond your period of stay in the United States (unless exempt by country-specific agreements). If more than one person is included in your passport, each person desiring a visa must submit a separate application.

2. Nonimmigrant Visa Application

Form DS-160 confirmation page – All applicants must complete and submit their own DS-160 form. The form may be completed online at https://ceac.state.gov/genniv/. Be sure to print out the confirmation page to bring to your interview.

3. Photograph

You will upload your digital photograph as part of completing the online DS-160 form. If you experience technical difficulties in completing the form, you may bring one printed photograph following these specific requirements: Format – JPEG digital format only Size – Must be at least 1200 pixels on the longest side with 300 dpi resolutionSubject headings – A recent passport-style photograph Face – Must show full face, front view with eyes open Hairline – Top of shoulders up Background – Must be plain light background without shadows Posture – Must have natural posture; clothes should not detract.

4. Application Fee payment receipt,

if you are required to pay one – Review our directory of nonimmigrant categories (https://travel.state.gov/content/visas/en/general/fees.html) to find out if an application fee is required for your nonimmigrant category

5. Support documents, as described below

– Evidence demonstrating financial ability during your stay in the United States (employer letter, bank statements from past year, tax returns from past year)

– Letter from employer specifying your position, salary and how long you have been employed there

– Evidence demonstrating strong ties to your home country (monthly mortgage or rental payments; ownership of property; evidence of immediate family members residing permanently in home country)

6. Any other documentation that may be requested during your interview

For example, if you plan to study during your time in the United States, you will need to provide evidence that you have been accepted into a US university or college as well as proof that you have sufficient financial resources to cover the cost of tuition and living expenses while studying here. Additional information about evidence that may be requested during your interview can be found on our website (https://travel.state.gov/content/visas/en/general/_requireme nts-documentation/_evidence-supporting-.html).

7. SEVIS I-20 or SEVIS DS-2019 form, if applicable

8. Certificate(s) of Eligibility For Exchange Visitor (J-1) status (if applicable)

9. Interested Sponsor Declaration For Exchange Visitor

(J1) status(s) (Form DS–2019), if applicable Please note that this list is not exhaustive and additional documentation may be requested during your interview appointment. We encourage applicants to bring any other documentation that might help demonstrate their eligibility for a nonimmigrant visa.

This concludes our list of required documents for applying for a nonimmigrant visa to the United States . We hope that this blog post has been helpful in outlining what you will need to gather before beginning your visa application process . Good luck!

Advice on Moving to the USA as an Immigrant or Expatriate

Everyone wants a piece of the American dream, but immigrating to the United States can be as intimidating as it is exciting. The United States is full of opportunities, but there are a lot of things you’ll need to do before you make the move.

You’ll need to secure the proper visa (or green card if you are looking to become a lawful permanent resident), decide what city to live in, find a job, and find proper housing. The cost of living varies in every region of the country. While there is a lot of information available, it can all be overwhelming.

To help you figure out which advice is most relevant to your particular situation, we put together this guide. Read on for advice on what you need to do to emigrate to the U.S. as an expat.

Quick Facts About the U.S.

The U.S. is home to over 321.6 million people, with the highest concentrations of expats living in New York, Washington D.C., and San Francisco.

The U.S. Dollar (USD) is the standard currency in all fifty states, and American English is the standard language in every region.

The second most common language spoken is Spanish (Español), but you’ll likely only hear it in cities and select towns.

If you move to a major city such as New York or Los Angeles, you’ll hear over 500 languages spoken by people from all around the world.

Unless you’re moving to a city with a high concentration of ex-pats from your native land, you’ll want to learn English. Most Americans expect everyone to speak American English. Learn to speak American English and your life will be much easier in the states.

How do Americans spend their leisure time? Most major American cities are thriving with art museums, music venues, bars, and restaurants.

Professional and college sports are also an American ritual nearly everywhere you go. Football, baseball, basketball, and hockey are favorites in every American household.

As for crime and safety, the statistics vary from state to state and city to city. In almost every state, you’ll find areas of high crime and neighborhoods with almost no crime at all.

Do your research to find crime statistics by zip code so you’ll know what to expect from your new home.

U.S Visas and Travel Documents Required of Immigrants

Temporary Relocation in the USA

There are a variety of different types of U.S. visas, so the one you’ll need will depend on your situation. Some of the most popular employment visas are the H-1B visa, the O-1 visa, and the F-1 Student visa.

If you plan to work in America and have a “specialty occupation,” you’ll need to complete an H-1B visa application for skilled workers. Specialty occupations need at least a bachelor’s degree in a specialized field.

You must have the appropriate degree to be considered for any job you apply for. This is one of the requirements you’ll need to meet to be able to apply for the H-1B visa.

The O-1 visa is for individuals with extraordinary talent in art, science, business, education, or athletics. It also applies to those who have made significant achievements in the television or motion picture industry.

There are different categories of the O-visa and requirements vary depending on what type of work you do.

Students looking to move to the U.S. will need an F-1 visa. With an F-1 visa, you can pursue a full-time academic career or seek vocational study anywhere in the United States.

In addition to work and student visas, there are also a variety of family-sponsored visas that can help you gain entry into the United States. Regardless of what type of visa you seek, you will need to meet all the requirements for that particular visa per your situation.

Once you know which visa is right for you, you’ll need to file the appropriate forms, pay an application fee, and schedule an interview. Different visas have different sets of rules and guidelines that you must follow.

Keep in mind, you’ll also need to file forms for employment authorization. If you’re moving to America for work, your prospective employer should be able to guide you through the process.

For a full list of immigrant visas and categories, click here.

Seeking or Applying for U.S. Citizenship

There are also several steps you can take to become a permanent citizen of the U.S. The first step in the immigration process obtaining a Green Card in order to declare permanent residency. In order to fill out the required forms, you’ll need to first determine your eligibility status.

Most people apply as a foreign relative, a foreign worker, or a refugee seeking asylum. Once you have a Green Card and the U.S. is your permanent residence, you can decide if you’d like to take the next step to naturalization.

Naturalization is the process through which a legal immigrant becomes a U.S. citizen. You’ll need to pass the naturalization test, but there are some things you’ll need to do before you can even take the test.

You have to hold a green card for a minimum of five years. In some cases, if you’re married to a U.S. citizen, you can take the test after three years. You must be at least 18 years old, and you need to be able to read, write, and speak English before having your interview and taking the test.

To become a naturalized citizen, the U.S. Government and Homeland Security require you to go through a ten-step process. You’ll need to determine your eligibility, fill out the proper forms, have your biometrics taken, and sit for an interview.

The final step in the legal immigration process is to take the oath of allegiance to the United States. If you’re serious about becoming a U.S. Citizen, keep in mind that it can be a lengthy process that takes a lot of preparation. For more information about applying for U.S. citizenship, click here.

The Cost of Living in America

The cost of living in the U.S. varies a lot from city to city. Expats can expect major cities such as New York, Washington D.C., and San Francisco to cost roughly the same—and they can be expensive.

Smaller cities and rural areas are much more affordable, but they offer fewer opportunities for employment. If you’re planning to move to a major city, here’s what you can expect to spend on the basic necessities.

According to MyNewPlace, the average one-bedroom apartment in New York City is $2,842 per month and the average two-bedroom apartment is around $3,600 per month. In San Francisco, the average one-bedroom apartment is $3,281 and the average two-bedroom apartment is around $4,431.

Monthly rent in major metro areas is high compared to other cities around the globe. For the same apartment in London, you would pay $2,178. Living in Sydney, Australia will cost you less than $2,000 a month.

These prices don’t include utilities, food, or basic living expenses. On average, you can expect to spend another $1,100 per month for that.

Food prices vary as well.

Lunch for two people at a mid-range restaurant in New York City or San Francisco will cost you $75. There is something for every budget, you just might not be able to live in certain areas if your budget is smaller.

One thing that people love about living in a major city is the ease with which you can get around. In New York City, a monthly transit pass costs $119 and offers unlimited access to subways and buses.

In San Francisco, the same monthly pass costs $73.50. Compared to other cities, this is quite affordable. A monthly pass in London will run you $170 each month.

Where you decide to live will dictate what your cost of living will be. Major cities cost the most, but if you consider moving just a few miles outside the center of a city, you’ll pay much less.

Smaller cities are typically more affordable and you can travel to bigger cities with ease.

For a more affordable cost of living, consider other cities such as Seattle and Philadelphia. In most of these cities, you’ll be able to find a one-bedroom apartment well under $2,000 per month.

In Seattle and Philadelphia you can expect to spend about $60 for a mid-range lunch for two and under $100 for a monthly transit pass. As with large cities, these cities have excellent transit systems that make it easy to get around.

U.S. Job Market

With the right skills, a strong resume, and the proper work permits, expats will find lots of opportunities in the U.S. job market.

Aside from exploring U.S. companies, many expats look for work with international corporations. You might also want to explore opportunities with an overseas consulate office that represents your native land.

According to Linkedin, the most popular jobs for college graduates in the U.S. are:

software engineer

administrative assistant

account executive

recruiter

financial analyst

marketing coordinator

research assistant

business analyst

account manager

project engineer

To find the U.S. career that’s right for you, visit usa.xpatjobs, Just Landed, and Indeed. With millions of jobs at your fingertips, you’re sure to find an opportunity that’s perfect for you.

Managing Your Finances as an Immigrant to the USA

As an expat, it’s crucial that you figure out your finances before moving. Do your due diligence by talking to your bank about transferring money.

Research what’s involved in changing banks. Always ask if there are banking fees involved or finance charges for U.S. transactions.

The rules and criteria for transferring money or opening a new account will depend on your current financial situation. In addition, make sure you know what your expat tax status will be.

Meet with a financial adviser or planner to learn how to manage your money and how to organize your current investments. If you plan to open a bank account in America, you’ll need a social security number, which will also be necessary for employment.

Depending on where you’re from, you may have the option to open an international account with the currency in U.S. dollars. Keep in mind that some international banks need you to maintain a minimum balance.

Understanding the U.S. Healthcare System

Unlike other countries, most hospitals in the United States are privately owned. There is no nationwide healthcare program or a federal government-owned medical system like you’ll find in Canada or Europe.

But this private operation of hospitals allows for the use of the best medical technology.

American medical facilities are world-class. Doctors are highly trained and often have multiple certifications. Many of the world’s best specialists practice medicine in the United States.

There are several advantages to the public health system. Wait times are short whether you need to make a doctor’s visit or schedule surgery. Specialists compete for patients, so you have a variety of options to choose from. The downfall is that these advantages often come with a hefty price tag.

Medical coverage in the United States is expensive, especially if you plan to pay out of pocket, so most Americans hold private international healthcare insurance. This insurance is usually provided by their employer or purchased through a private insurance agency.

Through healthcare programs, an employer may pay all or part of an employee’s medical expenses. What the employer does not pay, the employee has to cover on their own.

Even for healthy individuals, it is highly recommended that you hold some form of health insurance.

Best International Health Insurance in the USA for Foreigners

U.S. Schools and Educational Institutions

Navigating your way through a foreign school system can be intimidating and overwhelming. It’s essential that expats do ample research before deciding on what schools are right for their children or family members.

If you move to the U.S. with young children or teenage students, you may want to consider public education. As Government-funded institutions, public schools are much more affordable than private schools.

These schools provide educational resources to all students. The quality of public education varies, so decide what school district is right for you before you move.

There are other schooling options as well. In some areas, you’ll find magnet schools that focus on a particular course of studies such as engineering or the arts. Some cities have charter schools, which are partially funded by the government and partially funded by private donors.

Private schools are also an option and tend to provide better resources than other schools. But if you send your child to private school, you’ll have to pay tuition, which usually doesn’t come cheap.

If you’re looking to attend a college or university in the U.S., there are thousands of schools to choose from. Applying for college involves taking standardized tests, writing essays, and completing applications.

Different schools have different requirements and prerequisites for admission.

Once you are accepted at an American university, look for services that can help you make a smooth transition. Many American schools have resources to help expats adjust to their new environment.

Do Your Research

As with any big move, it’s crucial to do your homework before you decide where to go. Life in the United States is different in every city and every state.

Job opportunities may dictate where you go, but before you settle on a place to live, do your research. The cost of living can change drastically within a short distance.

Research schools to find the best opportunities. Understand the health care system and what that process looks like. Before you move, focus on your finances, establish bank accounts, and talk to a financial expert about your investments.

With so many great places to choose from, you’re sure to find an American locale that’s perfect for you and your family. When you do settle on an area to live in, connect with other expats to help you make the transition.

Search Facebook groups or MeetUp to find activities and events with other expats in your local area.

Moving to the U.S. offers excitement and opportunity, but it can be an overwhelming experience. Do your homework before you make the move so you know what to expect when you arrive.

Before you board a plane and move, make sure you have the proper visas and travel documents. You won’t be able to start your new life without them.

If you are moving to the USA (United States of America) from overseas and want a quick guide on how to get started, this article is just for you! This guide will help you find your way around in the new country, know what documents you need, and provide some tips on settling in.

You might be moving because of work or family reasons, or you’re an international student, or just because it’s time for a change. Whatever your reason, moving overseas can seem daunting, but it should go smoothly if you follow the simple steps outlined in this guide. We will discuss the various steps involved in moving to America, what you need to do before moving, and what to do once you get here in the USA!

What are the benefits of moving to the USA?

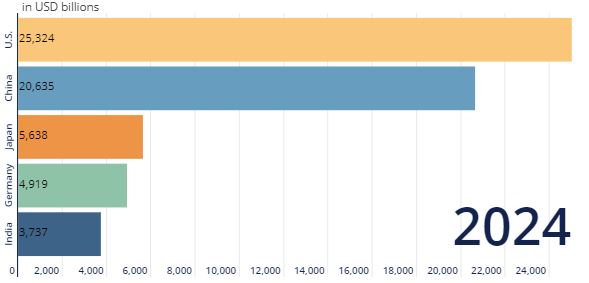

The American Dream is alive and well, and it’s available for anyone who wants it. Moving to America offers many benefits, the most notable being that moving to America means moving towards a better opportunity in the largest economy in the world.

As of 2019, United States’ nominal GDP was $21.5 Trillion and is expected to go up to $25.3 Trillion in 2024, making it the largest economy in the world measured by nominal GDP.

The United States has a free market economy that allows for nimble business investment and foreign direct investment. The United States is the world’s greatest geopolitical power, and it can keep a big international debt as the world’s primary reserve currency producer (US Dollars). The US economy is at the forefront of technology in many industries and is home to some of the biggest companies in the world in terms of valuation.

All these factors really make the USA the Land of Opportunity!

The USA is also a wonderful country with lots of different landscapes from deserts to beaches. The USA has some fantastic cities that are always bustling, but you can also live in more suburban areas and find peace if that’s what you’re looking for. So you can pretty much find whatever you are looking for in terms of lifestyle and location.

The following are the most notable benefits of moving to America.

Top 6 Reasons to Move to America:

More career opportunities for personal growth in the world’s largest economy

Relatively lower costs of living and owning a home relative to other developed countries

The best higher education system in the world

One of the best medical facilities in the world, leading to higher life expectancy

Diverse landscape, weather and natural beauty all around to fit everyone’s taste

Improved quality of life with USA’s economic strength coupled with affordability

US Visa – Everything you need to know

US Visa is an immigration document that allows you to enter the USA. You can apply for a US visa through the nearest USA embassy or consulate in your country. The US Department of State generally issues a US visa. However, it has an expiration date on its face, which will be anywhere from 6 months to 10 years depending on what type of USA visa you are applying for: tourist, student, work, etc.

You may not need a visa if you are a citizen or national of a Visa Waiver Program (VWP) Designated Country and are traveling to the United States for tourism or business for stays of 90 days or less.

What are the different US Visa Categories?

The USA visa application process varies according to the type of USA visa being applied for.

Here are the main US Visa categories for traveling to the United States:

1. Tourism/Visit and Temporary Business (B1/B2 Visa)

In addition, the United States issues tourist and visitor visas to individuals who wish to come into the country temporarily for business (visa category B-1), leisure (B-2), or both (B-1/B-2).

Examples of temporary business include attending business meetings or conferences and negotiating contracts.

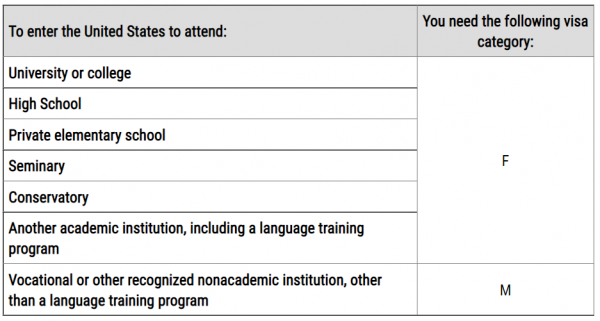

2. Study & Exchange (F, M, and J Visa)

The United States is one of the primary destinations for international students. To study in the United States, you must have a student visa. Whether you need an F or M visa depends on the type of school and program of study you wish to attend.

Exchange visitor (J) visas are nonimmigrant visas for individuals approved to participate in exchange visitor programs in the United States.

3. Employment (H, L, O, P, Q Visa)

Temporary work visas are for foreign nationals who wish to enter the United States to legally work for a specific length of time and do not qualify as permanent residents. Employment visas require the employer to submit a visa petition with United States Citizenship and Immigration Services (USCIS). An approved petition is required to apply for a work visa.

Here are the various categories of work visas in the US:

H visa: For professionals to work in a specialty occupation. Requires a higher education degree or its equivalent.

L Visa: For Intracompany Transferee to work for a current employer in a managerial or executive capacity or position requiring specialized knowledge in the US from their previous location overseas in an affiliate or subsidiary.

O Visa: For individuals with Extraordinary Ability or Achievement in the sciences, arts, education, business, athletics, motion picture, and television fields.

P visa: Artist, Entertainer, or Athlete visa

Q Visa: Participant in an International Cultural Exchange Program

What is U.S. Citizenship and Immigration Services (USCIS)?

USCIS oversees immigration to the United States and approves (or denies) immigrant and nonimmigrant visa petitions. You can check your US visa case status post your application process on the USCIS website.

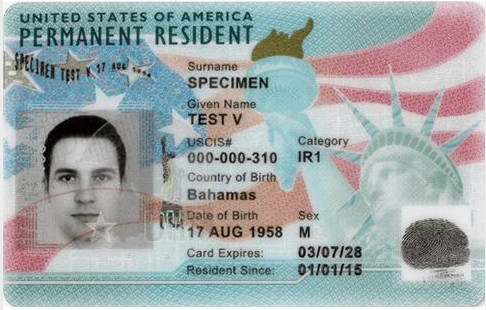

4. Immigration Visa (Green Card)

If you are interested in immigrating to the United States permanently, you will need an immigrant visa or what’s commonly referred to as a Green Card. The USA offers many different immigration visas or green card options depending on your specific situation.

There are five main types of US immigrant visa or Green card categories:

Family-Based Immigration – Green card for a certain family member(s) of U.S. citizens and lawful permanent residents (green card holders)

Employment-Based immigration – Green card for permanent residency and employment of temporary foreign workers and immigrant investors

Diversity Visa Lottery – The Diversity Visa Program (also commonly known as the green card lottery) annually makes a limited number of green cards available to individuals who fulfill certain eligibility requirements from nations with low immigration rates to the United States.

Special Immigrant Visa – Provides a Green card to various special categories, including former US government employees and their family member(s) in overseas countries and asylum seekers.

Adoption – An adoption green card issued for children from foreign countries who US citizens adopt.

After your immigration visa petition is approved, USCIS forwards it to National Visa Center (NVC) for immigrant visa pre-processing at the correct time. In addition, NVC will assist you in preparing your visa application for an interview for certain visa categories at US Embassies & Consulates.

5. Other Visa Categories

This includes all other visa categories such as transit visas, diplomat visas, etc.

US Visa Document Requirements

For most nonimmigrant visas, here are the required documents for applying for a US visa:

Other supporting documents such as Bank statements / Return Flight tickets / Employment letters etc. as applicable

How to get your US visa

Here is the step-by-step instructions for getting your US visa:

Check to see whether you require a visa or can take advantage of Visa Waiver Program

Select the type of US visa you will apply for based on your purpose of visit

Fill out the DS-160 form for a nonimmigrant visa.

Pay the application fee.

Schedule your visa interview.

Collect all your required supporting documents.

Attend your visa interview.

Wait until your visa is approved.

Moving to the USA Checklist: Top 11 Things to Do

Now that you have successfully gotten your US visa, it’s time to start planning for the big move and get you set up in your new home.

Here is the checklist of key things that you should do to plan your move, as well as keep in mind as soon as you arrive in the US:

1. Plan your move to America and understand your moving costs

Moving abroad can be a daunting task. But when done right, it can also be an exciting and fulfilling experience. Following are some of the key costs that you will have to keep in mind as you plan your move:

Hire a professional moving company or shipping service if you need to move a lot of stuff from your home country to the US. Packing your belongings is the first step to moving. Consider selling or donating extra items you no longer need.

Plan your travel well in advance to save on travel costs and maintain a list of important phone numbers and addresses.

Make sure you have all the mandatory immigration documents, required vaccinations for the USA.

Arrange your temporary accommodation for the first few weeks as you will need some time to find a place to rent or buy.

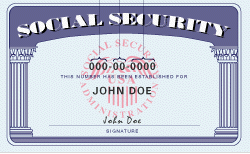

2. Apply for your Social Security Number (SSN)

Social Security is a federal program that provides social insurance for citizens of the United States. A US Social Security Number is a nine-digit number issued to identify and accurately record wages or self-employment earnings of US residents with a social security account. The Social Security Administration creates this account on behalf of the person when they accept work in the USA.

When moving to America, applying for a Social Security number as soon as you arrive is important because you will need it to get a job, collect Social Security benefits, and get other government services.

How can US non-citizens apply for SSN?

Only non-citizens authorized to work in the United States by the Department of Homeland Security (DHS) can get a Social Security number.

If you’re applying for an immigrant visa (green card) from your home country, you can apply for SSN along with your immigrant visa application and obtain your social security card before arriving in the US. Alternatively, you can visit a social security office in person.

Nonimmigrant visa holders can apply for SSN in two ways:

You can apply for your SSN on the same USCIS application Form I-765 (Application for Employment Authorization) if you are lawfully present in the United States and intend to seek work authorization from the United States Citizenship and Immigration Services (USCIS).

If you are currently in the US on a valid visa and your visa status allows you to work, you must go to a social security office in person to apply.

Required documents for US non-citizens to apply for SSN

First, the Social Security Administration will need your US immigration documents and valid foreign passport to validate your identity and work authorization in the US.

Following are acceptable documents:

• Form I-551 (Lawful Permanent Resident Card or Immigrant Visa)

• Visa stamp showing the class of admission that permits work in the US

• Form I-766 (Employment Authorization Document/EAD).

3. Open a US Bank Account

Many US Newcomers are unaware that some US banks allow US non-citizens to open a US bank account without SSN or remotely before arriving in the US.

When you move to America, you’ll need to open an American bank account to pay your bills and receive your salary. In addition, you should open a checking account with a debit card so you may pay for things without having to carry cash all the time.

The American bank account opening process will be different based on the type of US residency status you have currently, i.e., if you are planning to open your checking account without SSN from your home country before arriving in the US or if you have already obtained an SSN and are presently residing in the US.

Please refer to this detailed guide on how foreign citizens can open US bank accounts without SSN or remotely before arriving in the US and the best ways for opening bank accounts for foreign nationals after arriving in the US.

4. Obtain Driver’s License in the US

If you’re thinking about moving to the USA, a driver’s license is a must, and you should apply for one as soon as possible after arriving in the US. Not only will you need a driver’s license to drive in America, but it also serves as a primary local ID in the US.

You can apply for driving licenses by visiting the Department of Motor Vehicles (DMV) office near where you live or work.

Typically, the following documents are required for an application for a driving license for non-citizens:

Proof of Social Security Number depending on the state. Some states don’t require proof of SSN

Passport or other documents that serve as valid proof of identity

Proof of residence in the state, such as a utility bill or bank statements.

Photograph – a new picture will be taken at the DMV for your driver’s license.

Find out what kind of driver’s licenses are available in your state, and make sure to apply for the one that will best suit your needs, such as standard licenses and IDs, Real IDs, and Enhanced licenses and IDs.

5. Understand the American Healthcare System

Unlike many other developed countries where universal healthcare provides a basic level of coverage to all citizens, the US has a mixture of private medical insurance and two government-run programs known as Medicare and Medicaid.

Healthcare in the USA is expensive. Americans pay for their medical care either directly or indirectly through their health insurance in most cases. Therefore, ensure that you have a good medical coverage plan upon arriving in the US.

Here are the broadly three types of medical insurance coverage available in the US:

Private Health Insurance

Private health insurance is typically given through your employer or school, although you must purchase it individually if necessary. Your employer can either pay fully for your health insurance or ask you to cover a part of the premium.

Medicaid

Medicaid is a health insurance program used by low-income people, including families with children and pregnant women. It features a joint effort funded by taxes from the federal government and individual states.

Medicare

The Medicare program, administered by the United States government, is a tax-assisted health insurance plan and is available to older Americans over 65 years old.

Healthcare in the USA is expensive. Therefore, it is good to have one. If you have a job in the United States, your employer may provide health insurance benefits. To see if you are covered, speak with your employer to determine what options they offer and how much of that cost they cover. In addition to their contribution, they may ask for other contributions from you as well – so make sure you review all costs carefully.

Following is a glossary of keywords associated with American health care:

Premium: The monthly cost of your plan.

Deductible: The amount you pay out of pocket before your insurance benefits begin.

Co-Insurance: The percentage of expenses you’ll still have to pay after your insurance policy takes effect.

Co-pay: What you pay the doctor at every visit.

Important: Make sure you register with a Primary Care Physician (PCP) soon after arriving in the US. Your PCP will be your primary point of contact for regular medical needs, and they can refer you for any procedures or tests that need to be done.

6. Build US credit history

Many new immigrants and international students struggle to begin their new life in the United States with their credit score or credit history from their native country suddenly missing from the land of opportunity, America, which they now proudly call home. The US credit score determines your creditworthiness in the US and will be an important aspect of your financial life in the US.

Hence, it’s important to build and maintain your credit history in the US. Ideally, it would help if you started working on your credit as soon as you arrive in the US. The best and simplest way to build credit history in the US is to get started with a US credit card.

Refer to our detailed guide on How to Build Credit and get US Credit Card for New Immigrants & International Students.

7. Housing: Buying a House and Obtaining a Mortgage as a New Immigrant in the USA

Whether you’re coming to the US on a temporary visa for work or study or coming on an immigrant visa (green card), owning a house will be a dream come true. It’s always more cost-effective to own a home than to rent in the long run. You may use your monthly housing rental payments towards accumulating equity in a property that is increasing in value. Purchasing a home has additional benefits from an investment standpoint. It helps to accumulate wealth over time.

Contrary to what you might think, you do not have to wait two years or more to build a good US credit score before being eligible for home financing in the United States. In addition, some US lenders offer foreign national mortgages to US newcomers and Non-residents with no US credit history at competitive rates. This makes it possible and affordable for you to start researching your options to buy a house in the USA even before arriving.

Consult our comprehensive guide on how to get a mortgage as a new immigrant with no credit history in the United States.US Mortgages for Foreign Nationals & Expats

Buying a house in the US as a foreign national can be quite intimidating, especially if you are not aware of how the US real estate process works. If you’re considering buying a property in the United States as a US newcomer or as a non-resident foreign investor, this step-by-step guide will tell you everything you need to know about how to buy real estate in the United States from start to finish.

When you are ready to buy a house in the US either shortly after arriving (with the availability of home financing for newcomers) or after settling in the US; you should ideally work with a real estate agent who has expertise in working with foreign national clients, such as a real estate agent with CIPS designation.

A CIPS (Certified International Property Specialist) real estate agent has undergone specialized training to handle real estate transactions smoothly for foreign-born individuals residing in the US.

8. Understand your employee benefits in the US

USA’s employment benefits are among the best in the world, and it’s important to understand and take advantage of all the USA employment and employee benefits available to you as you move to America as a newcomer on a green card or temporary visas with a work permit.

Here are the most notable employment benefits in the US:

Health Insurance: Most employers in the US contribute towards an employee’s healthcare coverage. Employees usually pay a percentage of the total premium, but unlike most countries where you are required to contribute 100% towards health insurance premiums, USA employees typically have their share paid for by employers.

Paid Time Off (PTO): USA companies offer between 15-30 days off on average each year in addition to USA public holidays. USA PTO typically includes vacation days, sick leave, and paid federal/public holidays making it easier to plan out your time off in the USA.

401k Retirement Plan: USA companies offer 401k retirement plans that are funded by both employees’ contributions as well as company matching funds which is a great benefit for new immigrants moving to the USA.

Employee Stock Purchase Plan (ESPP): Some US companies offer stock purchase plans to employees which typically give them the opportunity to buy company shares at a discounted rate compared to what they are worth in the market.

When it comes to taking advantage of your employee benefits while living abroad, there is no better place than the USA, where your benefits will give you a strong footing for a new beginning in a new country.

9. Familiarize yourself with US Federal and State or Local Government Laws

As a US newcomer, you mustn’t get into any trouble with the law. However, you should become familiar with some common federal laws and state or local government rules as you settle in the US.

Apart from being a socially responsible US resident, make sure you follow some common laws that can be easily overlooked, such as traffic laws. For example, keep an eye on speed limits, always use your seat belt when driving, don’t drink and drive, etc. USA newcomers should also be aware of the USA’s federal laws, such as USA immigration laws, tax system, and labor laws.

10. US Education System

The USA has a world-class education system that can serve as an excellent foundation for any newcomer.

In the United States, primary education is divided into pre-school, kindergarten, elementary school, middle school, and high school. In most cases, children will attend separate primary schools, middle schools, and high schools located in the neighborhood. These are usually public schools, though there are many private schools and international school options available.

For higher education, the USA’s universities are among the best globally, and it remains one of the top destinations for international students.

11. Understand American culture and traditions

When you move to any new country, it’s only natural that you will try and build strong connections with the locals by understanding local culture and traditions. The US has a rich history of welcoming immigrants from different parts of the world. However, there may be certain cultures and customs that may be different than in your home country.

Research and embrace the US culture and learn about its customs, norms, and business etiquette. USA newcomers should also watch key US holidays and plan their social life around such events.

In Conclusion

The USA is a nation of immigrants and welcomes millions of newcomers every year with opportunities for employment, education, and entrepreneurship. USA’s history as the land of opportunity has given many new arrivals to the USA an opportunity at success in their pursuit of happiness here on American shores. No matter your background or where you’re coming from, there are always ways to start over fresh in the USA. Enjoy the United States, go around the country, spend time outdoors, and eat its delicious food and diverse cuisines. There is much to see and do here. We wish you the best in your new life in the US and hope you achieve your American Dream!

Select’s editorial team works independently to review financial products and write articles we think our readers will find useful. We earn a commission from affiliate partners on many offers, but not all offers on Select are from affiliate partners.

When new immigrants arrive in the U.S., they may have a difficult time securing a mortgage, a credit card or even renting an apartment. The credit score they had in their home countries typically won’t follow them to the U.S. because different countries use different methods for determining an individual’s credit worthiness.

Without a U.S. credit score, new immigrants typically struggle to access financial products available to those with long credit histories or who were authorized users on a friend or family member’s credit card.

Since a good credit score can give you access to better interest rates on a mortgage or better terms on your credit card, it’s essential to start building your credit score in the U.S. as soon as you can.

Ahead, Select explores some of the ways new immigrants to the U.S. can secure a credit card or start building their credit score when they have no credit history.

Cards you can get with a Social Security number

For starters, getting a credit card, paying your bills on time and in full and keeping your credit utilization ratio low are some essential ways to start building your credit history. However, new immigrants often face difficulty with the first step: signing up for their first credit card.

Depending on what type of identification new immigrants have, there are a few types of credit cards available to them. Most cards require that you have a Social Security number (and some require you to be a U.S. citizen), so your options will be more limited if you don’t have one.

If you have an SSN, you could be eligible for a secured credit card. A secured credit card requires that cardholders put down a deposit, which acts as collateral in case of default, that’s equal to the credit limit.

The Citi® Secured Mastercard® is one option available to immigrants who have an SSN or an ITIN (more on that below). This card makes Select’s list of best secured credit cards, because it allows you to take on a higher credit limit than your deposit, which can help you build your credit score. With the Citi Secured Mastercard, you can put down a deposit of $49 and get a credit line of $200. You’ll also be able to set your payment date so you can choose which time of the month is best for you to pay your bill. One drawback of this card is the lack of welcome bonus or rewards, but it’s not a bad choice if you’re not eligible for other secured cards.

Pros

No annual fee

$200 refundable deposit

Flexibility to change your payment due date

Cons

No rewards program

3% foreign transaction fee

What if you don’t have a Social Security number?

If you don’t have an SSN, you can use an individual taxpayer identification number (ITIN) to qualify for some credit cards. An ITIN is a form of identification issued by the IRS to foreign nationals for tax-paying purposes. Petal has two cards that are available to immigrants who don’t have an SSN: the Petal® 1 “No Annual Fee” Visa® Credit Card and the Petal® 2 “Cash Back, No Fees” Visa® Credit Card.

Both cards consider factors beyond your credit score when deciding if an applicant is eligible. When you apply, the issuer looks at your ‘Cash Score’ by analyzing your banking history, proof of income and on-time bill payments. If you sign up for a Petal 1 or Petal 2 Card, the issuer will consider your credit score if you have one. The Petal 1 Card offers a cash-back rewards program (2% – 10% cash back at select merchants), and the Petal 2 Card gives cardholders 1% cash back on all eligible purchases, then up to 1.5% back after 12 on-time monthly payments.

The Deserve® EDU Mastercard for Students is a good choice if you’re an international student without an SSN — you’ll need to be enrolled in college, have a U.S. bank account and be above the age of 18. The Deserve card also doesn’t have any foreign transaction fees, which makes it a solid option for international students planning to spend time abroad.

Rewards

Welcome bonus

Annual fee

Intro APR

Regular APR

Balance transfer fee

Foreign transaction fee

Credit needed

Another option is the Capital One Platinum Secured Credit Card. Much like the Citi Secured Mastercard, the Capital One Secured Mastercard, qualifying applicants can put down a deposit that’s less than their credit limit. You also won’t earn a welcome bonus or any rewards with this card. Cardholders can graduate to an unsecured card, but there’s no timeline for how long it can take.

What if you have a good credit history in your home country?

New immigrants from Australia, Brazil, Canada, India, Mexico, Nigeria, South Korea, and the UK might want to consider the program Nova Credit, which can translate the credit score that immigrants had in their home country to a U.S. credit rating through its Credit Passport® service.Misha Esipov, the CEO of Nova Credit, first founded the company with two other grad students at Stanford in 2015 when he saw international students struggling to secure a student loan or sign up for a credit card.

“Immigration is an incredibly vulnerable period of transition — you have to learn a new language, retrain professionally, adapt to a new culture — all in an environment where you don’t have the same social safety net you had in your home country,” says Esipov. “And it is precisely during this period of transition that the banking sector is inaccessible to millions of newcomers who arrive in the U.S. each year.”

Nova Credit is free for users and works by partnering up with banks, telecommunications companies and property managers that use the technology to determine an individual’s creditworthiness. One of Nova Credit’s major partners is American Express.

With Nova Credit’s partnership with American Express, immigrants from the UK, India, Mexico, Canada and Australia, who don’t have an SSN or an ITIN can qualify for a new credit card with Amex, which uses the Credit Passport® service to determine someone’s eligibility.

If you’re already an Amex card member from the UK, Canada, France or Australia, you can apply for another card through the Global Card Relationship. The Global Card Relationship allows you to maintain the Amex card account from your home country and the Membership Rewards points you’ve previously earned, according to Ashley Tufts, VP of corporate affairs and communication at Amex.

What if you don’t want to open your own credit card?

Lastly, new immigrants can opt to become an authorized user on someone else’s credit card. An authorized user is someone who can make purchases on a primary cardholder’s account but isn’t on the hook for paying off the balance.An authorized user benefits if the primary cardholder has a good credit score and continues to makes their payments on time and in full since their history is reflected on the authorized user’s credit report. Furthermore, if you have no credit history in the U.S., being an authorized user could have a big impact on your credit score because it serves as the foundation of your credit history.

“With the authorized-user strategy, there really is no downside to the person added as an authorized user. They have no liability for the debt, and if the primary cardholder abuses the account they can simply have their name removed from the card,” says John Ulzheimer, a credit expert formerly of FICO and Equifax. “The pros are that [new immigrants] may be able to get a credit card in good standing with a high credit limit and a low balance onto their credit reports.”

If you decide to become an authorized user on someone’s credit card, make sure to have a repayment plan with the primary cardholder. The primary cardholder can also choose not to give you your own card, but your credit history will still benefit.

Bottom line

When it comes to jump starting your credit history in the U.S., there are a variety of ways that you can do so. Depending on what type of identification you have, either a SSN or ITIN, you’ll have access to different credit cards.

If you have an SSN, getting a secured card is a smart first step that will allow you to graduate to an unsecured card in the future. If you don’t have an SSN, signing up for a credit card that doesn’t require a SSN, or becoming an authorized user on someone else’s credit card, are both good choices for establishing your credit history.

Petal cards are issued by WebBank, Member FDIC.

Editorial Note: Opinions, analyses, reviews or recommendations expressed in this article are those of the Select editorial staff’s alone, and have not been reviewed, approved or otherwise endorsed by any third party.

People in New York City, San Francisco or other cities that issue municipal IDs can often use those IDs as proof of identity.

2. Proof of address. Banks and credit unions often require proof of a street address to open an account. One of the following can satisfy this requirement:

Utility bill.

Lease.

Current driver’s license or municipal ID.

3. Identification number. An identification number means one of the following:

Any other government-issued document that proves your nationality or residence, such as a passport or foreign driver’s license.

Banks and credit unions may have requirements in addition to the ones listed above.

ITIN: What it is and how to get one

Don’t have a Social Security number? You can still get a bank account with an ITIN, or an individual taxpayer identification number.

ITINs are used by the Internal Revenue Service to process taxes. They’re available only to noncitizens in the U.S. who are not eligible for a Social Security number; their spouses and dependents can also obtain an ITIN. Here’s how to get one:

Fill out the required W-7 form, available in English and Spanish.

Mail in your application, take it to an IRS walk-in office or have it processed by an “acceptance agent.” These agents typically include colleges, accounting firms and financial institutions, such as banks or credit unions. Locate one near you on the IRS website.

Why should I open a bank account if I’m undocumented?

Personal safety

A bank account is a safe place to store your money. Even in the unlikely event that your bank is robbed, the money is insured and would be replaced. If you keep your money at home or on your person, you could lose your savings to theft.

Establish history

A bank account helps you build a financial foundation. In most cases, a bank account is required to open a credit card, buy a home or borrow funds to start a business, all actions that help establish a credit history. In some states, you can also open a college savings plan with tax benefits, known as a 529 plan, provided you have an ITIN.

Save money

With a bank account, you can cash checks or pay bills for free. A bank account also provides financial history, without which phone companies, apartments and other services can be more expensive or require larger deposits.

Credit unions and banks that don’t require Social Security numbers to open an account

Here are some banks and credit unions that don’t require you to have an SSN to open an account:

Bank of America.

Chase.

Marcus by Goldman Sachs.

Self-Help Federal Credit Union.

Latino Credit Union.

Large, mainstream banks such as Bank of America and Chase generally require about two pieces of documentation and proof of a valid U.S. street address. They also accept ITINs.

Some institutions, including some Hispanic American-owned credit unions, go out of their way to make the process smoother for immigrants.

Self-Help Federal Credit Union for example — which has branches in California, the Greater Chicago area, Milwaukee, Florida, Virginia, North Carolina and South Carolina — accepts the following forms of identification:

Valid driver’s license.

Passport.

Matrícula consular (identification card from a Mexican consulate).

State-issued ID.

Military ID .

Residency card.

Another financial institution known for helping immigrants, Latino Credit Union in North Carolina, accepts:

Government-issued ID from any country.

Valid ITIN or Social Security number.

Proof of current address.

Latino Credit Union and Self-Help FCU also offer products designed with the immigrant community in mind. DACA and citizenship loans, for example, are available to help members cover the cost of a deferred action or naturalization application.

Identification requirements vary from bank to bank, and credit union to credit union, so call ahead or stop by a branch location to find out what documents you need to open an account. If language is a barrier, ask if the bank has a representative who can help you in your native tongue.

About the authors: Kelsey Sheehy is a personal finance writer at NerdWallet. Her work has been featured by The New York Times, USA Today, CBS News, and The Associated Press.

Amber Murakami-Fester is a former banking writer for NerdWallet. Her work has appeared in USA Today and The Christian Science Monitor.

If you’re planning on living in the United States on a permanent basis, there are a few things you’ll need to do as soon as — if not before — you arrive. If, for instance, you don’t already have a job, you’ll need to find one. And with that new income, you’ll need to have a place to put your money, which means you’ll need to open a U.S. bank account.

With a bank account in place, you’ll be able to do things like:

Set up automatic withdrawals for rent and utilities

In this article, we’ll cover the basics of the setting up an account at a U.S. bank, how to write a check, and how to schedule automatic withdrawals.

Opening an Account

U.S. banks will generally allow non-U.S. citizens to open an account but may not grant the same permissions to someone who fails either the green card test or substantial presence test. If you have a green card, then you’re in the clear. Otherwise, you’ll likely need to pass substantial presence test.

To pass this test, you must have lived in the United States for:

31 days in the current year, and

A total of 183 days during the past 3 years — that’s including the current year plus the two years prior. To tally this total, you can count all the days you lived in the United States in the current year but only ⅓ of the days from the previous year and ⅙ of the days from the year before that.

To be clear: it may still be possible to open an account even without a green card (or any documentation, for that matter). You will, however, need to have an Individual Taxpayer Identification Number (ITIN) and a U.S. address, at minimum. Ultimately, you’ll want to contact the bank to see what their policy is in this regard.

Documents

If you think you’re eligible, then you’ll need to gather certain information and documents to open an account. These generally include:

Cash deposit: Anywhere from $25 to $100

Your name, phone number, and address(es)

A social security number (SSN). If you don’t have an SSN, you could opt to use an ITIN

Utility statement containing U.S. address

Two forms of government-issued ID. Examples include:

Your passport with the visa inside

Driver’s license, whether U.S. or foreign

Work I.D. card issued in the United States

Retail credit card

This is just a general list, and different financial institutions may have different requirements, so be sure to call ahead of time. If you don’t have a green card or a Social Security number, you may have to actually go to the brick-and-mortar bank, rather than apply online. But, again, requirements will vary depending on the financial institution.

If you’re eligible for a Social Security number but haven’t gotten one yet, read our guide on the subject to learn more about the process.

Applying for an ITIN

To apply for an ITIN, you’ll need to submit IRS Form W-7, your immigration status documents, and proof of identity — together with your federal income tax return. You can use any of the following options to apply:

Submit via U.S. mail to the Austin Service Center (see below)

Attend an appointment at an IRS Taxpayer Assistance Center

If submitting via U.S. mail, you can send your documents to the following address:

Internal Revenue Service

Austin Service Center

ITIN Operation

P.O. Box 149342

Austin, TX 78714-9342

Once you successfully obtain an ITIN, you won’t need to go through this process again. You can file your income tax return according to the normal filing instructions.

Writing a Check

To write a check in the United States, you need to fill in all the appropriate spaces. In the following section, we’ll explain how to fill out a check, working from the top to the bottom.

Write today’s date. It’s important that the bank knows when the check was filled out. There’s a difference between a check written in 1986 and one filled out last week.

Specify the check’s recipient.You’ll want the bank to know who this check is for. You can write the name of the person (or the company) on the line next to the phrase, “Pay to the order of.”

Fill in the amount using digits. After you write the recipient’s name, you should find a box to the right with a dollar sign next to it. Write the numeric amount — $50.30, as opposed to “fifty dollars and 30/100” — in this box.

Fill in the amount using words. On the next line down, you will need to write the amount with words — “Fifty dollars and 30/100”, as opposed to $50.30. Even if you’re writing an even dollar amount (without cents), you should still include the fraction. So, if you’re writing a check for $50.00, you should still write “Fifty dollars and 00/100.”

Include a memo. At the bottom of the check, you should see a section marked “memo.” Here, you have the option to write the purpose of the check. If, for instance, the check is for rent, you can write “Rent for August.”

Add your signature. Finally, on the remaining line, you will need to sign your name, telling the bank that you agree to pay the amount specified above.

Once the check is complete, you can hand it over to the recipient, who should then be able to cash it at their financial institution.

Setting Up Automatic Withdrawals

Having a U.S. bank account will allow you to set up automatic payments for any recurring (or one time) bills. If setting up automatic withdrawals via your bank, you’ll need the pertinent information for the payee, including their address and account number, which you can usually find on the most recent bill. If you’re using the payee’s website to set up the transaction, you’ll need to provide your account and routing numbers.

Where will you find these numbers? You can simply look at your checks. Each check should contain the routing number (which identifies the bank), your account number (which specifically identifies your bank account), and a check number (which helps you keep track of the number of checks you’ve written).

Each number will be listed in succession at the bottom of the check. The routing number is first, at the bottom left, and is 9 digits long. The other numbers will be to the right, though they may be in any order. Just know that the account number is the longer number.

Remember, every financial institution is different, so you’ll need to do some research ahead of time. The bank website is usually a good place to start. They’ll usually have a help section containing a list of questions or topics to guide you. Alternatively, you can call the bank directly, though you may end up having to wait on hold before speaking to a representative.

If you’re looking to move to the United States, but you’re having trouble getting started, reach out to Boundless today.

Understanding basic banking and finance — and the terminology people use to talk about them — can make a big difference in your bank balance.

Here are 10 banking terms you should know to manage your money better.

1. Routing number

A nine-digit number that identifies your financial institution. Larger banks may have multiple routing numbers that are based on the geographic location where the account was opened. (Read more about routing numbers and how to find yours).

2. FDIC

The Federal Deposit Insurance Corp. A government-run organization that insures customers’ bank deposits up to $250,000 if the bank fails. The National Credit Union Administration is the equivalent for credit unions.

3. Certificate of deposit

Commonly known as a CD, an account into which you deposit a sum of money and agree to keep it there for a specified length of time. The account typically pays higher interest rates than standard savings and checking accounts.

4. APY

Annual percentage yield. The amount of interest you gain from keeping money in an account in a year, including compound interest. (Want additional details? Read more about why securing a high APY is important for your savings.)

Make the most of your cash

Track all your spending at a glance to understand your trends and spot opportunities to save money.

5. APR

Annual percentage rate. The amount of interest you gain from keeping money in an account in a year, not including compound interest. In the context of a loan, the APR represents the cost of borrowing money.

6. Compound interest

Interest that applies to the original deposit as well as any newly earned interest. For example, if you put $100 in an account that earns compound interest at 5% a year, in the next year you will earn 5% on $105. Noncompounding interest would continue to earn 5% on $100.

7. Savings account

Typically, an interest-bearing account used to hold money for short- or long-term goals or emergencies. You can add to this account at any time, but certain types of withdrawals may be limited to six per month.

There is a wide range of interest rates available for savings accounts, and online banks tend to have higher rates than national banks.

8. Returned item fee

A bounced-check fee charged to the person trying to deposit the check. It can be charged if there are insufficient funds in the check writer’s account or if the account is closed.

9. Overdraft fee

A fee incurred when your checking account doesn’t have enough funds to cover a payment that is requested. The financial institution will pay what your account lacks, after which your account may have a negative balance. (Here’s more information on how much banks charge for overdrafts.)

10. Checking account

An account at a financial institution into which you can deposit money and from which you can write checks for purchases. Most people use checking accounts to receive their wages and pay their bills.

Financial institutions may be awash in jargon, but this glossary of banking terms should help you understand even the most confusing of concepts.

The economic disruption caused by various lockdowns around the world has had an unusual impact on the financial services industry: it is accelerating digitization. For example, banks have been on the frontlines to help administer loans and quickly get cash to businesses and individuals in financial distress. But while some banks and financial institutions are enabled to serve customers remotely, others are feeling exposed because they simply don’t have the digital identity capabilities to engage with customers in a physically distanced world.

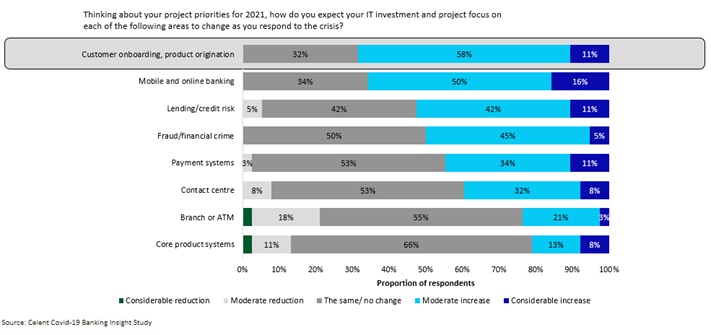

With the initial shock of the coronavirus pandemic over, banks are moving beyond business continuity issues and focusing on their 2021 investment agendas, including digital transformation. In a recent web seminar, Celent’s Head of Retail Banking Practice, Zil Bareisis, cited results from the Celent Covid-19 Banking Insight Study, which highlighted that enhancing digital self-serve capabilities, improving digital onboarding, and reducing operational efficiencies were top priorities for banks. The same study illustrated that most banks plan to increase their IT budgets for customer onboarding and product origination initiatives to respond to changing consumer preferences and habits (see figure 1 below).

Figure 1. IT investment and project focus for banks in 2021

What Does Successful Digital Onboarding Look Like?

Successful customer onboarding in the digital channel needs to deliver on three major requirements:

Customer experience (CX): CX remains a top driver for digital onboarding initiatives at banks, because the ultimate goal is new customer acquisition. This applies to all digital channels and all steps in the customer journey – from identity verification and consent capture to onboarding and ongoing account access and transactions.

Cost effectiveness: It’s not enough to deliver a great CX. Banks also need to ensure they leverage the latest remote onboarding technologies to deliver operational efficiencies in the front and back office.

Regulatory compliance: The digital account opening process includes steps such as identity verification that are tied to Know Your Customer (KYC) regulations. These regulations differ from country to country and need to be accounted for, especially when operating across borders. The good news is that most countries now allow organizations to verify identities remotely as long as the technology has strong fraud detection controls in place.

Modern Identity Verification Is Essential to Improving the Onboarding Experience

With an increasing number of applicants reluctant to go to a bank branch to open a new account, digital identity verification has become a key requirement to enable remote account opening and onboarding experiences. The goal is to ensure that the applicant claiming the identity is in fact the true owner of that identity and is genuinely present during the process. Customer identity verification is also a key ingredient for ongoing fraud monitoring.

Today, banks are increasingly implementing document-centric identity verification techniques. Gartner’s Market Guide for Identity Proofing and Affirmation cites that, “by 2022, 80% of organizations will be using document-centric identity proofing as part of their onboarding workflows, which is an increase from approximately 30% today.” This category of solutions enables organizations to:

Capture the ID document: Capture a photo of the applicant’s passport, driver’s license, or other identity document – typically via a mobile device.

Authenticate the ID document: Analyze the ID document to assess signs of tampering or counterfeiting and ensure authenticity. For example, examine the MRZ zone, the expiry date, the font, and the color of the document to ensure that these components are consistent with a real ID document.

Verify the applicant against the ID document: Compare the photo of the document with a “selfie” (facial biometrics) taken by the applicant submitting the document. Test for the genuine presence of the applicant using “liveness detection”, which identifies whether the presented biometric trait is from a live human or is being spoofed by a digital or manufactured representation.

Banks must also ensure that the agreements are legally binding and admissible in a court of law, because the account opening process is fundamentally an agreement process. To achieve this, we recommend implementing e-signature to capture intent and a step-by-step account of the process.

Because abandonment remains a key challenge in the onboarding process, banks are increasingly relying on more than one identity verification capability to ensure applicants can complete the process in a single-sitting. This includes selecting a vendor with strong identity orchestration capabilities and connections to third parties for identity verification, as well as redundancy through workflows that include failover techniques in the event of latency or downtime.

Digital Identity Spans the Entire Lifecycle of the Customer

Digital identity plays a critical role across all steps in the customer onboarding process – not simply the verification step in upfront account opening process. The lines between identity verification, authentication, and fraud detection are blurring with respect to the techniques that can be used to increase trust in affirming an individual’s identity and identifying fraudulent activities. We’re starting to see a continuum between these capabilities and also seeing the increased ingestion of data across the lifecycle of the customers to stop fraudulent activities during and after the account opening process.

Adapting identity verification and subsequent authentication to risk is essential for the delivery a smooth and secure customer experience. The good news is that banks now have access to machine learning-based technologies with the ability to ingest contextual and behavioral data about customers, the devices they use, and the transactions they carry out to assess risk. Depending on what the customer is trying to do, risk-based assessments and scores can be used to drive intelligent workflows that trigger actions (i.e., re-authenticate the customer) to then stop fraud from taking place.

Final Thoughts

Because nearly every aspect of modern life today embraces remote channels, the need to obtain confidence in the identities of consumers, partners, and employees through remote interactions continues to grow. Government entities like the Financial Action Task Force (FATF) agree that if done right and if appropriate risk measures are in place, the risk of transacting in a non-face-to-face environment can actually be lower than the identity and authentication techniques that banks and other financial institutions have traditionally deployed in the branch.

Watch our webinar with Celent’s Head of Retail Banking Practice to learn about the pressing identity verification and authentication issues that are front and center in today’s remote world and best practices for connecting remote applicants to real identities.

Rahim Kaba is a passionate and results-driven digital technology leader who has played a key role in advancing digitization initiatives at organizations around the world. As VP Product Marketing at OneSpan, he leads the go-to-market strategy of the company’s growing portfolio of solutions.

Opening a U.S. bank account as soon as you arrive will help you transition much more quickly to your new surroundings. It can help you pay the bills, send and receive money transfers, deposit paychecks, and set up a mobile wallet. Fortunately, opening a United States bank account is a fairly straightforward process.

This guide is especially for new arrivals like immigrants and international students, but it’s also relevant to anyone who needs a U.S. bank account.

Let’s look at the requirements and a brief step-by-step guide to opening an account in the U.S.

Documents You Need to Open a U.S. Bank Account

Keep in mind that banking regulations may differ from state to state — which is to say, specific requirements will depend on the location of a bank or credit union.

Because there may be additional requirements depending on your residency status, opening an account online may not be a widely available option.

Most times, talking directly to someone at a physical branch is your best bet.

That being said, most financial institutions require the following documents:

Some form of government-issued ID like a passport or U.S. green card;

Social Security number;

Immigration forms; and,

Proof of physical address like a utility bill or apartment lease agreement.

Again, documentation requirements differ depending on where you open your bank account, so it’s best to speak with customer service before applying for an account.

Opening a U.S. Bank Account as an International Student

International students with a valid student ID and supporting documentation should be able to open an account. Check with your university for recommendations and banking resources. Brown University, for instance, offers a comprehensive online guide to foreign students on opening a U.S.-based account.

Not all banks allow international students to open a bank account, but if they do, they may require the following types of documentation:

Your address in the U.S. and one in your home country

Government-issued passport

Verification of school enrollment

A secondary form of identification such as a driver’s license, student ID or birth certificate

Opening a bank account can be a simple process once you understand what you need. Here are the general steps you’ll need to take.

1. Gather Your Documents

Using the list above, gather all documentation you’ll need to open a bank account. That way you can ensure a faster and smoother process when you fill out an application online or in person.

2. Choose the Type of Account You Want

The bank account you want will depend on your individual needs and reasons for being in the U.S.

For instance, international students are likely to prefer basic bank accounts and ones that charge minimal or no monthly maintenance fees.

Immigrants or non-residents who plan to stay in the U.S. permanently may want to open a joint savings accounts with their spouse or investigate accounts for investing.

Whatever your reasons, most non-residents are looking at either a checking or savings account as a starting place. Both make it easier for you to send money abroad and to conduct everyday transactions.

A savings account tends to have higher interest rates so you can earn some money on your deposits. However, due to Federal Reserve Regulation D, you may not be allowed to make over six withdrawals a month.

A checking account allows more frequent transactions and offers other features such as a debit card for purchases and the ability to pay bills online.

However, you may earn less in interest. Check fees before starting, such as non-network ATM charges or bank transfer fees. Some checking accounts may require a minimum balance.

Once you figure out which type of account you want, you’ll need to look up different financial institutions to see which ones can best fit your needs.

3. Choose a Bank and Confirm Requirements

Given the sheer amount of banks and accounts to choose from, it can feel overwhelming to figure out the best option. Ideally, you want a bank or credit union that understands the needs of newcomers or international students.

For instance, most major banks have dedicated bank accounts for college students, such as the Chase College Checking Account. Keep in mind you’ll need to be physically in the United States to open such an account.